The Four Phases of Your Financial Life

This post was last updated on 31 May, 2023, to reflect all updated information and best serve your needs.

This post was last updated on 31 May, 2023, to reflect all updated information and best serve your needs.

It’s helpful to break your financial life into phases so you can focus on what’s most important right now. Understanding how decisions you make today affect what tomorrow looks like is vitally important. Keep in mind, these phases blend together and don’t always look the same as someone else’s journey.

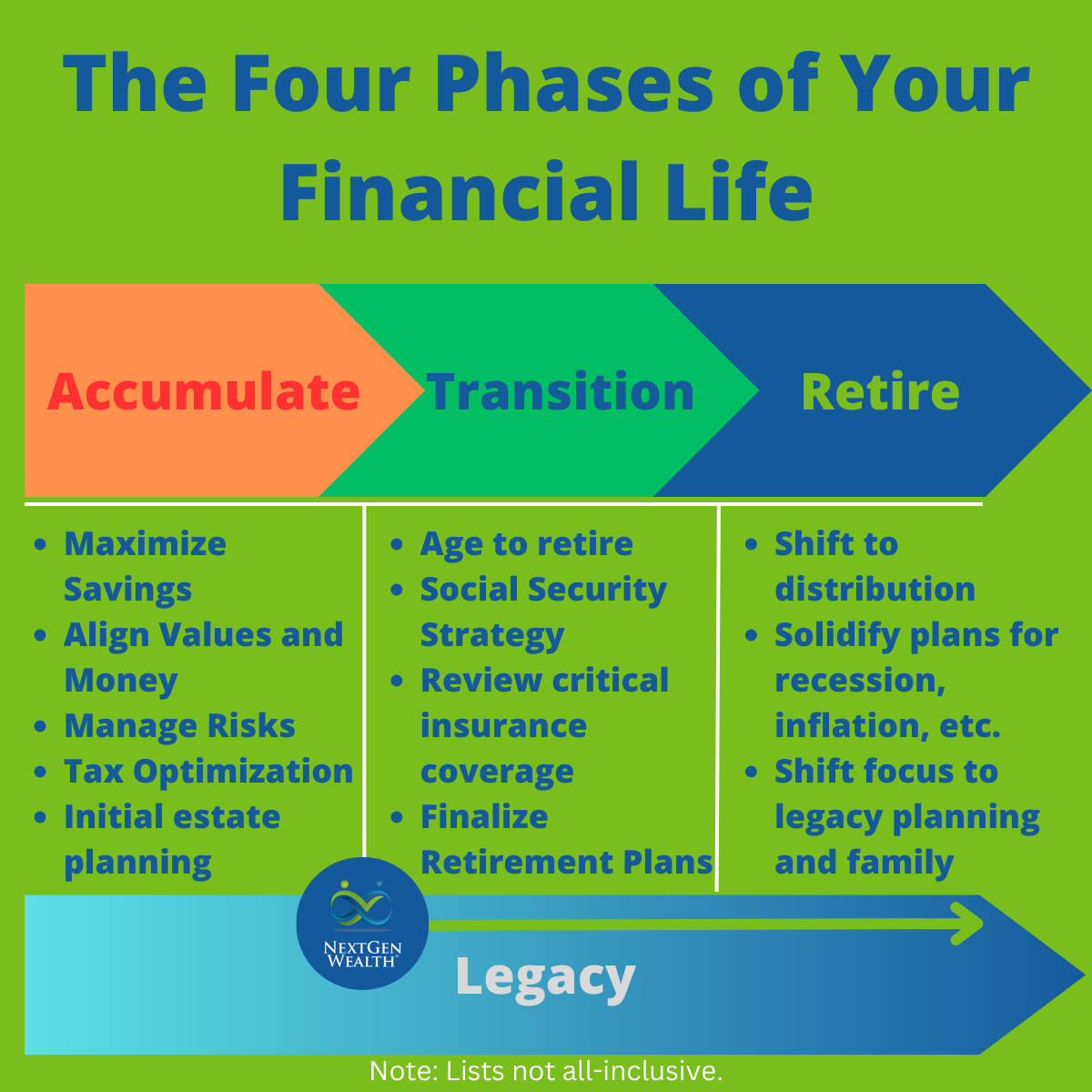

By having a better understanding of each phase, you’ll be able to know what to expect and plan throughout your retirement. We’ll break things down into four phases:

- Accumulation

- Transition

- Distribution

- Legacy

Keep in mind, you might have to revisit pieces of each phase as you plan for other phases. This is especially true when we’re talking about legacy planning. The way you structure things as you accumulate wealth and transition into retirement has a substantial impact on legacy planning considerations.

The Accumulation Phase

A coordinated approach to saving, investing, risk-management, and tax optimization can set the foundation for a smooth transition into retirement. You should take advantage of saving and investing opportunities early. The earlier you start saving, the less you actually need to contribute to your retirement accounts.

Align Your Career, Money, and Values

Aligning your career with your values and financial expectations can be incredibly impactful on your mental health, physical wellbeing, and your long-term financial success. If you make less, but are happy to work longer, this could be better than making more, being miserable, and retiring earlier. You need to strike the right balance for you.

Healthy Savings Rate

Ideally, you’ll want to save as much as possible across tax-deferred, tax-free, and taxable accounts. You still need to have some fun, but it’s a lot easier to spend more money in retirement than it is to produce more income.

Maximize your savings for future withdrawal needs. Decisions to maximize Roth accounts (if eligible) and completing Roth conversions could have a great impact on Required Minimum Distributions (RMDs) and save on taxes later. It’s a lot easier to accumulate retirement savings in the right place to start (if possible) than go back later and move things around.

Accumulating growth in unrealized gains: if you have an ESOP or profit-sharing plan at work, keeping an eye on possible Net Unrealized Appreciation (NUA) strategies could be really helpful too.

Managing Risk

Managing the financial risk of an untimely death or disability is critical. Nobody wants to think about the death of a spouse, but if something terrible happens, you don’t want to add to the hurt with financial issues on top of everything else. Having proper insurance (medical, life, and long-term care) is critical when the unexpected happens.

Portfolio Risks

Building a properly diversified portfolio doesn’t just mean buying a bunch of different stocks and bonds. You need to properly balance the risk you’re willing to accept to achieve the gains needed to support your retirement.

Health and Longevity

Making a healthy lifestyle part of your long-term strategy can have an immense impact on your future. Adopting healthy habits earlier in life can greatly reduce health scares and medical costs in the future.

In the accumulation phase, you’ll want to at least have basic wills and trusts in place. You aren’t going to know exactly what assets you’ll have later in life, so a detailed estate plan might not be possible yet. However, you can start laying the groundwork now.

This is also a great time to start thinking about philanthropy and if you’re interested in any type of charitable giving.

The Transition Phase

NextGen Wealth specializes in helping you transition into retirement. Transitioning from the accumulation phase to generating a sustainable income is critical to your long-term success in retirement. The objectives of this phase are to design a strategy to define what you want life to look like in retirement, minimize taxes, and be prepared for changes as they occur.

When to Retire

Helping you decide exactly when you want to (or when you can) retire is a key first step. There’s not a set age you need to retire, but there are several age-specific things you need to be aware of. We’ll help you work through all those items.

Helping you create the best Social Security strategy for you and your spouse (if you’re married) is a key piece to this equation too. There’s a lot to know about Social Security, Medicare, and how the rest of your financial life can affect Medicare premiums. If you are married, taking a step back and looking at all the income and insurance options available to both of you can help a lot.

At the end of the transition phase, you’ll have all the big pieces in place and have a much clearer picture of what the next phase of your journey looks like.

Optimizing Your Retirement Tax Strategy

Taxes never stop, and we never stop helping you save on taxes either. We want you to pay all the taxes you’re supposed to and nothing more. We integrate tax planning throughout our time working with you.

Creating a Health and Wellness Plan

You’ll want to ensure you have a plan you can share with your family. Whether it’s a decision regarding what type of care you want as you age or final burial arrangements, you need to make sure everyone is on the same page.

You need to review your life insurance and determine your additional needs (if any) as well as decide on long-term care insurance or any other risks you may face.

As you exit the transition phase, you’ll make decisions regarding where you want to retire and how you’ll spend your time. We should have you on a path to a fulfilling and healthy retirement.

The Distribution Phase

In the distribution phase, you’re likely going to have a set income and will have to manage things a little differently. You’ll be switching from saving in retirement to using those savings to produce consistent retirement income.

Problems Always Occur

You’re going to encounter “issues” like down markets and inflation. We put quotation marks around the word issues because inflation and recessions are something we should expect. We plan for this. The news makes it seem like inflation and recessions are a big surprise, but they’re not. We’re not letting those things knock you off course.

Optimizing Income

It’s important to identify and optimize all income sources such as pensions, non-portfolio (1099) income, rental income, and any other sources. These assets need to be withdrawn in the most tax-efficient manner.

Creating an order of operations is helpful too. There are many different tax considerations here as well. It can be a lot to keep track of, but you can’t ignore the effects of taxes as you withdraw money to funds your retirement.

Also, developing and implementing a charitable giving strategy may be a key component of your income strategy. If philanthropy is one of your goals, charitable giving can be a helpful way to save on taxes at the same time.

The Legacy Phase

It’s tough thinking about “the end” but we’ve all got a legacy we’ll leave behind. The most important parts of your legacy won’t have anything to do with money. However, we still need to do something with your assets.

Communicate Your Wishes

Creating and sharing your legacy and estate plan with your family is critical. Ever have a family member pass leaving confusion and fighting afterward? One of the best gifts you can give is eliminating confusion for the people you’ll leave behind.

We highly suggest planning your financial life around your family – not the other way around. However, there’s a lot of legal and tax implications to what you want to happen.

Optimizing the Transfer of Wealth

It’s critical to understand how assets will transfer at the death of each spouse. We’d probably all prefer to avoid spending even one minute without our significant other, but rarely does it work out that way.

You want to make sure your assets go where you want them to. Whether you want your remaining assets to go to specific people or a charity, you need to make sure all the proper legal paperwork is ready to ensure your wishes are carried out. This eliminates confusion and ensures there’s no guessing on the part of your heirs.

Estate Tax Optimization

You’ll probably need to consider the tax rates of your heirs, trust beneficiary designations, naming a charity as a beneficiary, and other unique aspects. You don’t want to pass on an asset to your loved ones and accidentally create a tax burden for them.

There are also ways to transfer wealth while you’re still living so you can see the impact of your giving. This could take the form of paying for college tuition of a grandchild, funding a charitable event, or something else.

Regardless, your estate plan needs to remain up to date and reflect your values and wishes.

Bringing Everything Together

Overall, all the phases build upon one another to form the whole picture of your financial life. With thoughtful planning, you can ensure your values are represented in the way your finances are handled while reducing financial stress throughout your lifetime.

At NextGen Wealth, we take you through our COLLAB Financial Planning Process™ to help you define what you want retirement to look like and how to achieve your dreams. Contact us today to schedule your retirement checkup!

This article was written by

This article was written by