Critical Ages to Keep Track of in Retirement

This post was last updated on March 28, 2026, to reflect all updated information and best serve your needs.

You might not care much about what age you are, but the government does. It’s very important you keep track of key age-related milestones in retirement. If you fail to properly plan for these, you may be missing out on some opportunities – or even face penalties.

As you enter the end of your working years and transition into retirement, these key dates are critical. You really need to start paying attention to these in your 50’s and 60’s. Once you’ve reached your 70’s, the actions tied to your age start to taper off, but there are other important factors to consider.

Table of Contents

- Critical Ages by Decades

- Catching Up in Your 50's

- Setting Plans in Your 60's

- Settling Down in Your 70’s and Beyond

- Required Minimum Distributions

- Keep Track and Plan Ahead

- Working with NextGen Wealth Through the Decades

Critical Ages by Decades

The easiest way to keep these straight is to split things up by decades. This also helps tie these age-related checkpoints to the three main phases of retirement planning: accumulation, transition, and decumulation.

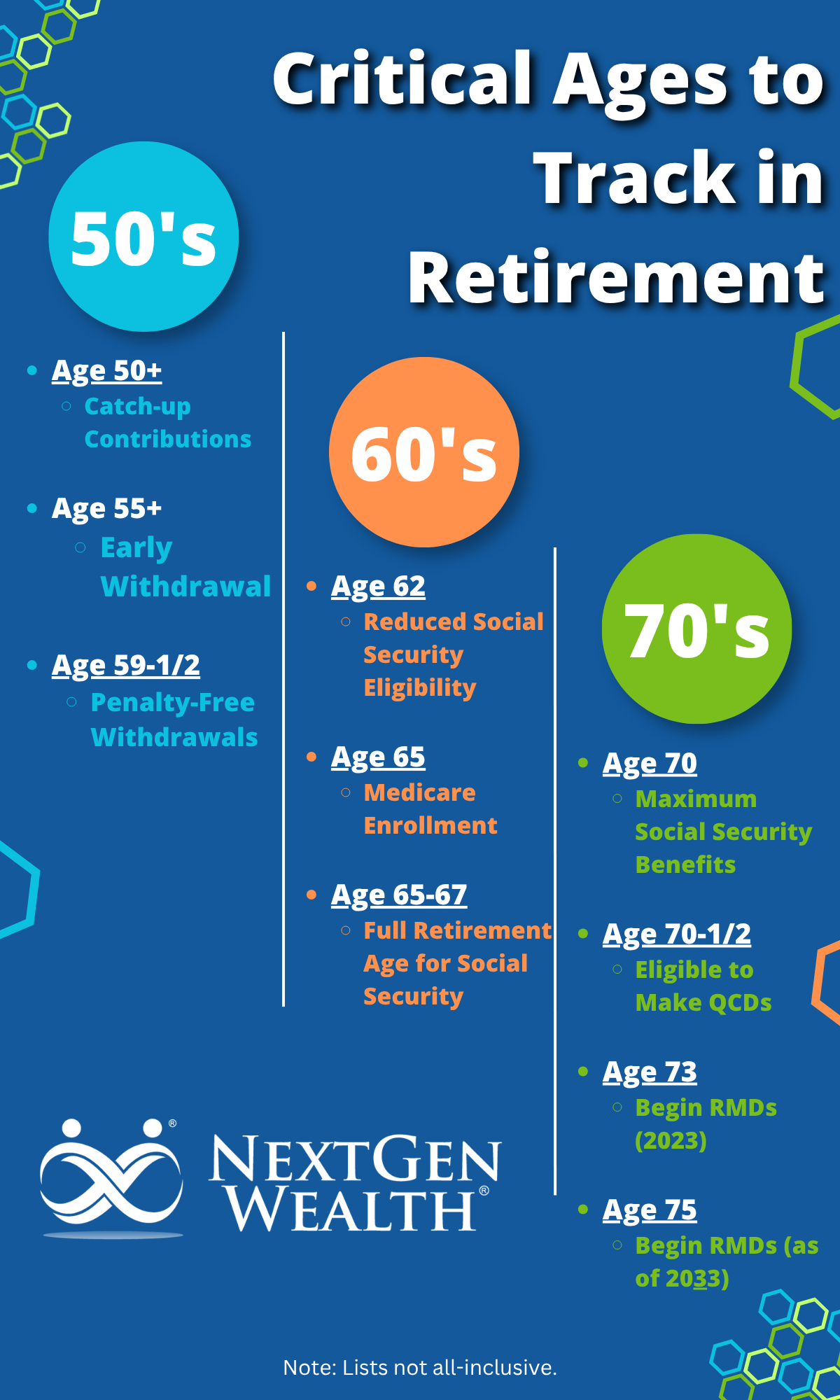

Catching Up in Your 50's

Starting the day you turn 50, you’ve got a few different things you need to consider. You’ll be eligible for catch-up contributions and, at the very end of your 50’s, penalty-free withdrawals. You’re likely making more money than ever, and you may be thinking about what the right age to retire is for you.

Catch-up Contributions

It’s highly likely you’ll be in your peak earning years in your 50’s. You’ll also be able to contribute more to your retirement accounts via catch-up contributions. The catch-up contributions change, but the opportunity to "top off" your retirement savings is valuable regardless of what they set it at.

Employer Plan Contribution and Catch-Up Limits

For 2026, you can contribute up to an additional $8,000 in your 401(k) or an extra $1,100 in your IRA. Actually, there's even more you can contribute after age 60. For those aged 60 to 63, you can contribute an additional $11,250 to your 401k, 403b, or 457 plan instead of $8,000. Instead of the normal maximum contribution of $24,500, you could put up to $32,500 or $35,750 (age 60-63) per year into your 401k, 403b (maybe more), 457, or Thrift Savings Plan (TSP).

Other Unique Catch-Up Opportunities

403(b) plans also have an additional 15-years of service catch-up contribution limit. We won’t go into detail here, but there's also a lifetime limit for the 15-year catch-up. Depending on your years of service and previous contributions, you will eventually exhaust the ability to make these additional 15-year catch-up contributions.

Individual Retirement Accounts

On top of your retirement account through work, you can also contribute extra money into an IRA or Roth IRA. For IRAs, you can contribute $7,500 per year as well as an additional $1,100 catch-up contribution for a total of $8,600. You might not be eligible to contribute to a Roth IRA directly, but you can still contribute to a regular or traditional IRA.

Limits for [Not So] SIMPLE IRAs

Catch-up contributions for SIMPLE IRAs are not very simple. The SIMPLE IRA contribution limit is $17,000 ($18,100 for 10% increase), and catch-ups are limited to an additional $4,000 ($3,850 if eligible for the 10% increased limit). The catch-up is $5,250 if you're age 60-63.

The additional 10% contribution increase is determined based on your employer's non-elective contribution percentage and the number of employees receiving $5,000 or more of compensation per year. In short, it's anything but "simple." You can read more from the IRS or contact your plan administrator for more information.

Open a Roth IRA and Start Thinking About Roth Conversions

Although there isn’t a specific age you need to have a Roth IRA, by the time you’re in your 50’s you probably need to open one. You want to start the 5-year clock and start researching Roth conversions, which are also subject to the 5-year rule.

The 5-year rules say distributions from a Roth IRA are not considered “qualified” unless 5 taxable years have passed. Simply put, if you contributed to a Roth IRA for tax year 2026, you cannot take earnings out without penalty until 2031. You can still withdraw your contributions, not conversions, without penalty or tax before age 59-1/2.

Return of Roth IRA Contributions is Tax-Free

The return of your contributions (not rollovers) to a Roth IRA are not subject to the 5-year rules and are not penalized for early withdrawal. Under the Roth IRA distribution rules, your contributions should always be taken out first.

Roth IRA Rollovers Are Subject to the 5-Year Rule

Roth conversions are subject to a slightly different 5-year rule. Unlike your direct contributions to a Roth IRA, any amount you convert to Roth will be subject to the 5-year rules and the 10% early withdrawal penalty. You’ll also have to pay taxes on the earnings. This can get a little complicated because amounts from rollovers are distributed from your Roth IRA second, after your contributions.

Each Roth conversion has its own “clock” for the 5-year rule. For instance, if you complete Roth conversions for 5 years from 2025-2029, you have 5 separate 5-year rule time periods with the last one starting in 2029.

Ability to Withdraw Penalty Free

As you close out your 50’s, you’ll be able to make withdrawals from most retirement accounts penalty-free. Once you reach age 59-1/2, you don’t have to worry about the 10% early withdrawal penalty. Now you’ll be able to use the money you’ve been saving for retirement, which will be here before you know it.

Additionally, if you have an employer plan and retire after age 55, you can make withdrawals penalty-free. This "rule of 55" exception to the early withdrawal penalty can be really handy for people looking to retire before age 60.

Setting Plans in Your 60's

Your decisions in your 60’s are probably the most important to your retirement success. The decisions you make immediately before and during the transition into retirement are absolutely critical. This is why NextGen Wealth puts so much emphasis on the transition phase of retirement planning.

At this point, you’ll probably be putting a lot of thought into exactly when you want to retire – or when you can retire. You’re going to reach many important milestones during this major decade of transition.

Social Security Eligibility

Beginning when you turn 62 years old, you can start drawing reduced Social Security benefits. However, you want a solid Social Security withdrawal strategy to maximize your benefits. For the most part, once you start drawing Social Security, there’s no changing it.

Depending on when you were born, you’ll reach the normal or “full retirement age” between 65 and 67 years old. Most retirees should wait to draw Social Security until full retirement age. As a matter of fact, for many people, waiting to draw Social Security even later is the most beneficial option.

The way Social Security benefits are calculated is complex and confusing. However, you can pull your estimated benefits directly from the Social Security Administration. This is a great starting point for the Social Security conversation.

Medicare Eligibility

Being ready to enroll in Medicare is very critical. Not only is it a benefit you earned, but if you sign up too late, there could be permanent penalties you’ll have to pay. You can use the questions on the Medicare.gov website or ask your financial advisor to determine when you are eligible.

Open Enrollment for Medicare

For most people, Medicare eligibility starts at age 65. You have a 7-month enrollment period to sign up for Medicare without a penalty. The initial enrollment period is the 3 months prior to the month you turn 65, the month you turn 65, and the 3 months after the month you turn 65.

In other words, if your birthday is on July 4th, your enrollment period is from April 1st all the way through October 31st. If you get enrolled in Medicare during those 7 months, you’ll have one less thing to be scared of for Halloween!

If you’re continuing to work past 65, then you may not need to enroll in Medicare yet. However, for many people, gaining Medicare eligibility is the last piece of the puzzle to get their retirement started. Healthcare is always important – especially for retirees.

Settling Down in Your 70’s and Beyond

Things may slow down a bit in your 70’s, but there’s still plenty to keep track of. For most of us, we’ll already be retired or retiring soon. However, even if you choose not to retire yet (or ever), there are still some critical ages you need to pay attention to.

Maximum Social Security

If you turn age 70 and you still haven’t started drawing Social Security, it’s probably time to start. There's no increase in your monthly payments by waiting beyond age 70. Unless there is a very unique circumstance, it’s time to go ahead and start drawing your maximum Social Security benefits.

Qualified Charitable Contributions

Qualified charitable contributions (QCDs) might not be a huge deal for you. However, for folks who have charitable giving as part of their financial plan, it could be. At age 70-1/2, you are eligible to take distributions from your retirement accounts as QCDs.

Required Minimum Distributions

Once you reach your mid-70’s, you’ll have to take required minimum distributions (RMDs). These have changed significantly over the years. However, with the changes from SECURE 2.0, almost everyone will have to start taking RMDs at age 73 or 75 (starting in 2033).

You definitely want to pay attention because if you don’t take the required distributions, you’ll be subject to penalties. You’ll have to pay a 25% penalty on the amount not taken out. For example, if you failed to take your RMD of $10,000, you’d have a penalty of $2,500. However, if you correct this in a “timely manner,” the penalty is lowered to 10%.

Keep Track and Plan Ahead

As you can see, there are many different milestones tied to your age as you get closer to retirement. Many actions you take will affect others. For example, Roth conversions in your 50s and 60s may help avoid RMD issues later.

If you fail to plan for all these different pieces of your finances, you could be unknowingly setting yourself up for heartache in the future. Fortunately, you can prevent many problems down the road through proper financial planning.

Working with NextGen Wealth Through the Decades

For over a decade, NextGen Wealth has specialized in the transition period, covering the 5 years prior to retirement and beyond. If done correctly, everything will line up and go smoothly. Our goal is for you to enter retirement knowing you crossed all the t’s and dotted all the i’s so you can enjoy a worry-free retirement.

Contact us today to schedule your no-obligation financial assessment and see if we're a good fit for your situation.

This article was written by

This article was written by