Are Annuities Subject To RMDs?

Annuities and required minimum distributions (RMDs) are some of the most confusing and buzzworthy topics in retirement. But do you need to worry about either one? Maybe, maybe not.

Annuities often create confusion because of their complexity and the high-pressure sales tactics used to get you to buy them. RMDs are annoying because nobody wants to be forced to do anything in retirement, let alone pay taxes on top of it. It’s important to understand what type of annuity you’re talking about, whether RMDs are going to be an issue for you, and what alternatives you might have.

Table of Contents

- Understanding Required Minimum Distributions

- Required Minimum Distributions for Annuities

- Qualified Annuities Are Subject to RMDs

- How RMDs are Calculated for Annuities Inside Retirement Accounts

- Fully Annuitized Accounts Already Meet RMD Requirements

- Using Annuity Income to Satisfy RMDs for Partially Annuitized Accounts

- Aggregation of RMDs

- When RMDs Begin

- Non-Qualified Annuities Are Not Subject to RMDs

- Special Situations and Exceptions: QLACs

- Common RMD Mistakes with Annuities

- Bottom Line on Annuities and RMDs

Understanding Required Minimum Distributions

If you’re not familiar with required minimum distributions (RMDs), they’re a forcing mechanism to get you to pull money out of your retirement accounts and pay taxes on the money you’ve saved. If you’re forced to take more out than you’d need, RMDs will affect your retirement by raising your overall tax bill. For many retirees, their normal retirement income withdrawals will satisfy their RMD for the year.

Purpose of RMD rules

The government’s stated reasoning for RMDs is to prevent people from avoiding taxes forever. In other words, Uncle Sam is okay with you delaying taxes until retirement, but not skipping out completely. Whether you pay taxes now or later, there’s no escape.

The concept of RMDs was originally established in the Tax Reform Act of 1986 (pdf page 380 if you’re curious). There have been several changes since then.

When RMDs Begin

Originally, the starting age for RMDs was 70-1/2. However, this has been modified several times, and SECURE Act 2.0 raised the RMD age to age 73 or 75, depending on when you were born.

Failure to Take Your RMD

The penalty for failing to take your RMD is now a 25% excise tax on any amount not withdrawn. So, if you were required to take $10,000 and withdrew $6,000, you’ll owe $1,000 for the $4,000 you failed to withdraw on top of taxes when you actually withdraw the money. However, if you correct the mistake in a “timely manner,” you can reduce the penalty to 10%.

Accounts Typically Subject to RMDs

Not all retirement accounts are subject to RMDs. Now, only non-Roth “qualified” plans such as 401ks, 403bs, and IRAs are subject to RMDs. This also applies to the Federal Thrift Savings Plan (TSP). Always check with the IRS to see if RMDs apply to your situation.

Inherited retirement accounts are also subject to RMDs. There are specific rules regarding inherited retirement accounts, depending on who inherits the account and whether RMDs have already started.

Accounts Not Subject to RMDs

Most accounts, aside from tax-deferred retirement accounts, are not subject to RMDs. This includes Roth IRAs (during the owner’s lifetime), regular checking and savings accounts, and non-qualified investment accounts. However, there may still be estate taxes and other considerations to contend with.

Required Minimum Distributions for Annuities

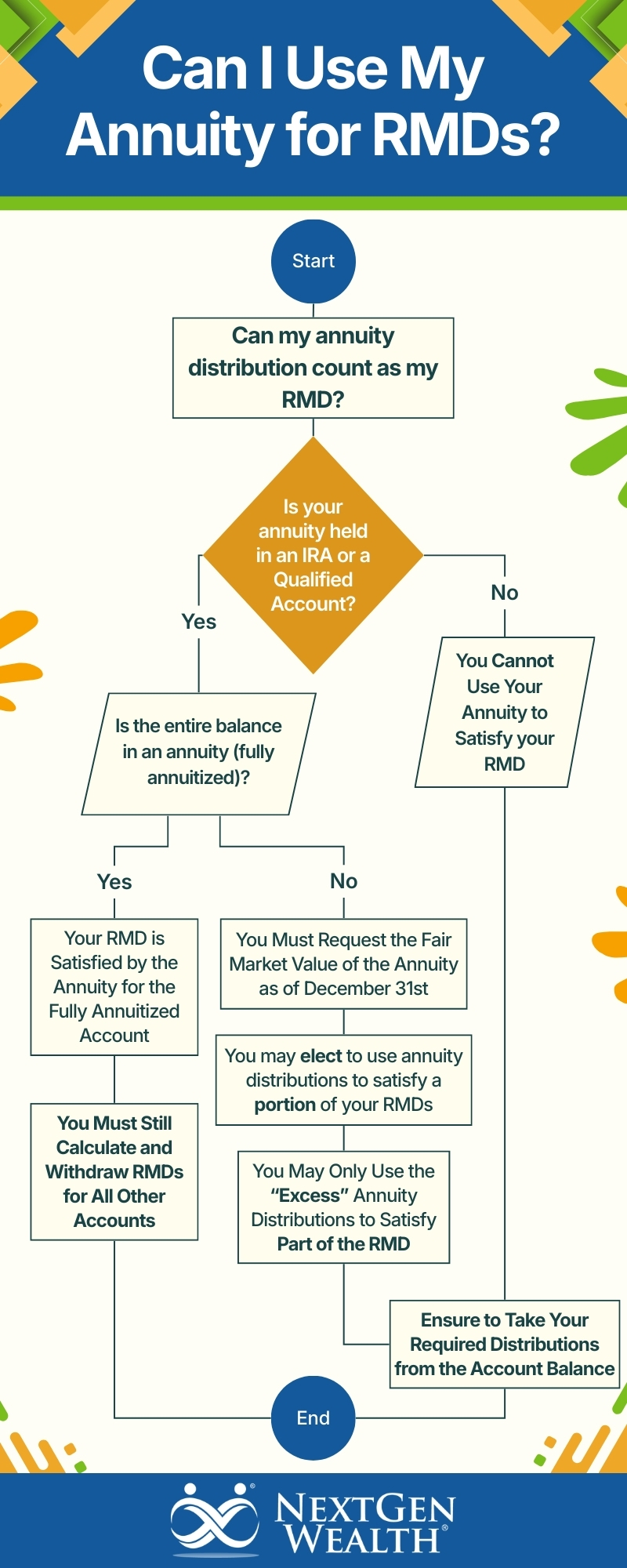

It’s a little confusing to think through when an annuity is subject to RMDs. The annuity itself isn’t subject to RMDs. However, the account used to purchase the annuity can trigger RMDs.

In other words, annuities themselves aren’t automatically subject to RMDs, but if you use pre-tax money to purchase the annuity, it would be. This is why annuities are characterized as either qualified or non-qualified.

Qualified Annuities Are Subject to RMDs

The term “qualified” annuity refers to an annuity purchased with pre-tax retirement funds. In other words, if you bought an annuity inside your 401(k) or IRA, or “annuitized” your IRA or retirement account, it would be subject to RMDs.

How RMDs are Calculated for Annuities Inside Retirement Accounts

In general, all RMDs are calculated using the account balance as of December 31st of the year prior and your life expectancy. Your account balance is divided by your expected life expectancy to determine your RMD. In theory, you’ll be forced to distribute your entire account during your lifetime.

Fully Annuitized Accounts Already Meet RMD Requirements

Because annuities are distributed during your lifetime, they’re deemed to satisfy your RMD if the entire account is annuitized. If your entire IRA or other retirement account is used to purchase an annuity, it will already meet RMD requirements.

However, this only applies if the entire account is used to purchase the annuity. If you used only part of your retirement account to purchase the annuity (partial annuitization), the remaining portion must have RMDs calculated and dispersed.

Can You Get 100% on This Retirement Quiz? Spoiler: Most people fail this 5-question quiz.

Using Annuity Income to Satisfy RMDs for Partially Annuitized Accounts

A new provision in SECURE Act 2.0 allows you to use distributions from a qualified annuity to satisfy the RMD for the non-annuitized portion of the account. However, you would need to calculate the RMD for the annuity separately from the RMD for the non-annuitized portion of your account. Then you can count distributions from the annuity toward the account's total RMD.

The catch is you’ll need the insurance company to give you a fair market value calculation of your annuity each year to determine the RMD for the value of the annuity and determine the “excess” portion. This excess portion can be applied to your remaining RMDs for the account.

Aggregation of RMDs

If you have multiple retirement accounts subject to RMDs, you must calculate the RMD for each account separately. However, you can combine the value of your IRAs (aggregate) and take all your RMDs from any one of your accounts as long as the total equals the sum of all your RMDs. A larger withdrawal from one account would be counted toward the total value of all your IRAs for RMD purposes.

In other words, each account must calculate its own RMD, but the IRS treats all your IRAs as a single pool. Bottom line, the more accounts you have, the more you have to keep track of. The financial institution administering your retirement account should provide you with the RMD calculation each year.

When RMDs Begin

Currently, RMDs begin either when you turn age 73 or age 75, depending on when you were born. You must take the first distribution by April 1st, the year after you reach RMD age. The catch is that you must also take your RMD for the current year.

So, if you turned 73 this year, you need to take an RMD for this year, but it’s not due until next April. However, you also have an RMD next year as well. If you delay, you’ll have a doubled-up RMD for next year.

Non-Qualified Annuities Are Not Subject to RMDs

Separate from annuities purchased with pre-tax retirement funds, you could purchase an annuity with other assets. These annuities purchased with after-tax money are considered non-qualified annuities. Since these aren’t purchased with pre-tax money inside a qualified retirement account, they’re not subject to RMDs.

However, the rules governing the taxation of non-qualified annuities can be complicated.

Special Situations and Exceptions: QLACs

Qualified Longevity Annuity Contracts (QLACs) are an interesting exception to RMDs. In short, a QLAC is a special type of annuity with its own rules, regulations, and forms. These are often touted for their ability to defer RMDs until age 85.

The catch is their restrictive nature. These are very illiquid. Also, unless you pay extra for a return-of-premium or guaranteed payment period option, your money is gone if you pass away before you start receiving payments. It’s best to only put money into a QLAC if you plan to live past age 85.

There are also limitations on the maximum amount you can purchase in a QLAC. These are a special type of annuity designed with longevity concerns in mind.

When QLACs Make Sense

A QLAC might make sense if you’re concerned about running out of money. Although they could help with RMDs, it’s not a primary reason you’d purchase a QLAC. In fact, if you’re going to have an RMD problem, you almost certainly don’t have a high risk of outliving your money.

However, these could be beneficial in certain instances. If the fear of running out of money in your late 80’s and beyond is a concern, then a QLAC might be a suitable option.

Common RMD Mistakes with Annuities

Besides not fully understanding if you need an annuity, there are some other common mistakes.

Assuming Annuities Satisfy Your Entire RMD

One of the biggest potential RMD mistakes with annuities is assuming annuity payments automatically satisfy your RMDs for your IRA or retirement account. As mentioned earlier, you have the option to use excess annuity distributions to satisfy your RMD. However, this isn’t automatic.

You must request the fair market value calculation and determine the portion of your RMD the annuity distribution satisfies. Then you still have to withdraw the remaining RMD.

Misunderstanding Tax Treatment of Withdrawals

Distributions from qualified annuities are taxable as ordinary income. You can’t forget about this when you start taking other RMDs. You could end up paying more in taxes than you wanted. This constant stream of taxable payments can also limit your ability to complete Roth conversions to help with your overall RMD amounts.

Bottom Line on Annuities and RMDs

Annuities themselves are not automatically subject to RMDs. The type of account the annuity is held in is the deciding factor. More importantly, there’s a good chance you don’t need the complexity and costs associated with annuities in the first place.

Before you worry about RMDs or annuities, it’s important to understand where the annuity fits in your retirement plan, if at all. Think twice about getting advice from someone who sells annuities. The incentives to sell them often outweigh the long-term benefits to you.

How NextGen Wealth Can Help

At NextGen Wealth, we take an objective view of your entire financial picture. We start with what you need to meet your goals, then recommend the tools best suited to your situation. In other words, we start with your goals and work backward. We don’t use high-pressure sales tactics and don’t sell any insurance products.

If you’d like to see how working with a fee-only, fiduciary can help you in retirement, contact us today to schedule your no-obligation financial assessment.

This article was written by

This article was written by