Important Retirement Plan Contribution Deadlines for 2026

This post was last updated on February 04, 2026, to reflect all updated information and best serve your needs.

Make the most of your retirement planning in 2026! No matter how much time there is between now and these deadlines, mark your calendar so you don't miss anything. Now is the time to prepare for retirement account contributions (or withdrawals).

There are always new rules to consider, as well as old regulations affecting your contributions and potential tax burden. Here's what you need to know about retirement plan contribution deadlines for 2026.

Table of Contents

Contributing to Your 401k Plan

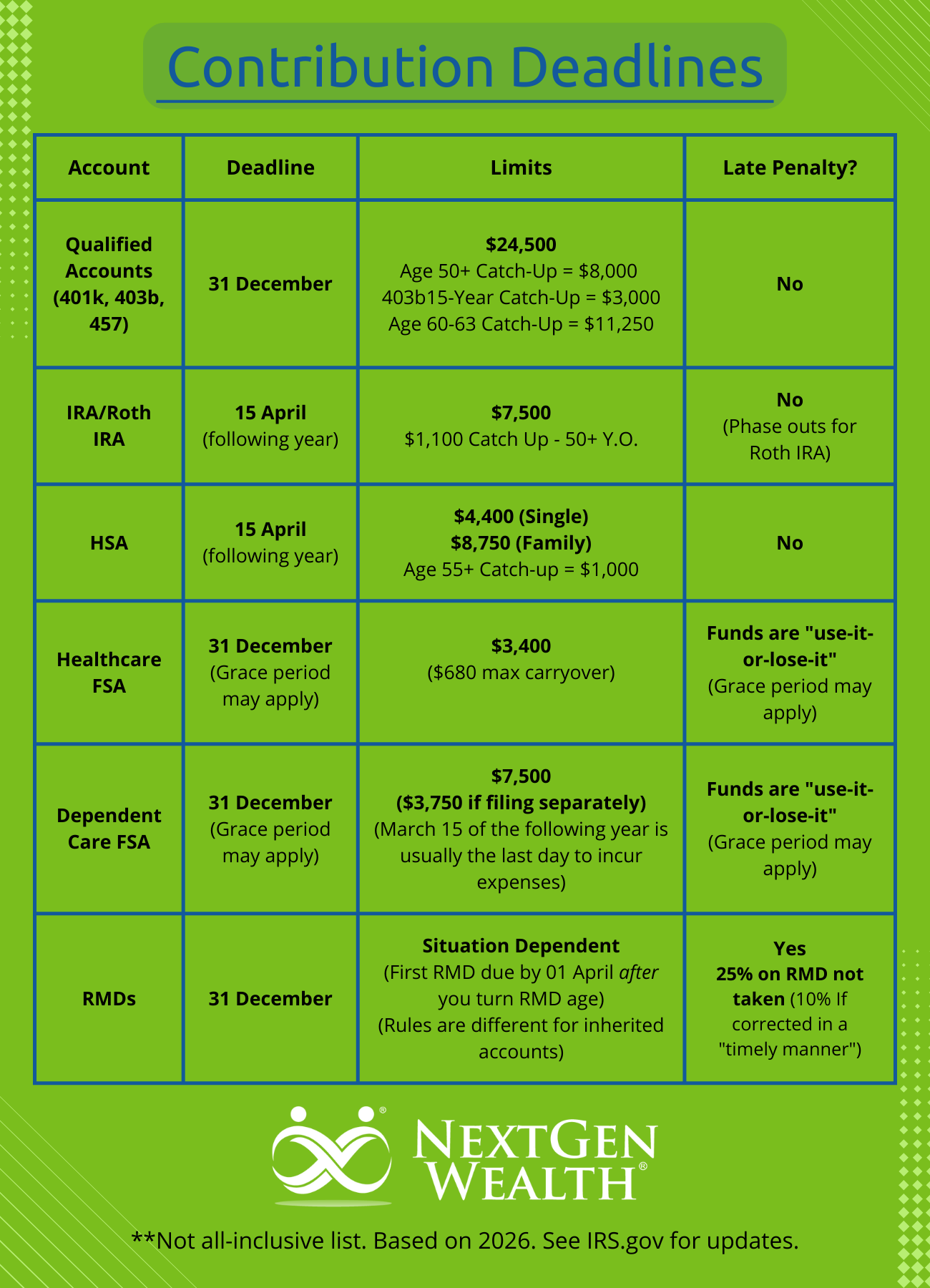

Your 401 (k) is one of the most effective options for saving for retirement. With a sizeable annual contribution limit ($24,500 in 2026), this is a great way to maximize your retirement savings goals.

If you’re at least 50 years old, you can add another $8,000 to your total, bringing your total contributions to $32,500 for the year. If you're age 60 to 63, your catch-up limit increases to $11,250 for a total of $35,750 you can stash away for retirement.

The deadline to contribute to your 401(k) for the year is December 31st. Make sure you have your payroll deductions adjusted to ensure you're getting the most out of your plan.

Maximize Your Employer Match

If you get an employer match, you'll want to spread your contributions out over the year to take advantage of "free" money from your employer. Technically, you earned it regardless - you may as well get the match.

If you spread your contributions evenly over the whole year, you can ensure you're getting your match. If you hit the max in July or August, you'll miss out on the matching contributions for the remainder of the year. You want to be right on time, not too early and not too late.

To do this, you'll want to determine how much you can and want to contribute for the year. Then divide it across 12 months, and you’ll know how much to elect for salary deferral.

Regardless, if you haven’t adjusted your contribution amounts in a while, you might not be maxing your 401k - even if you were a few years ago. Most plans allow you to set it to max so you won't miss out on bumping up your contributions each year.

Contribution Deadlines for IRAs

Individuals can contribute to an IRA until Tax Day, April 15th, of the following year. In other words, you have until April 15th, 2026, to make your final IRA contribution for tax year 2025.

This means you can contribute to your IRA or Roth IRA after you know your total income for the year. This is especially helpful if your income includes year-end bonuses or if you have significant seasonal income toward the end of the year. Also, waiting to contribute helps ensure you don’t contribute to your Roth in error if you’re close to the Roth IRA contribution eligibility phaseouts ($153,000 - $168,000 filing single or $242,000 - $252,000 for married filing jointly for 2026).

The maximum amount for IRA and Roth IRA contributions is $7,500 ($8,600 for those 50 and over). So, if you haven’t reached the limit for last year, you might want to take one final look before tax time and decide if you want to contribute. Overall, this deadline gives you a bit more flexibility when planning for retirement savings.

Health Savings Accounts and Flexible Spending Accounts

If you have a Health Savings Account (HSA) or Flexible Spending Account (FSA), make sure you’re maximizing these benefits.

Health Savings Account (HSA) Deadlines and Limits

HSAs are a great tool for saving for medical expenses during your working years and into retirement. You must make contributions by April 15th of the following year (April 15th, 2026, for 2025 contributions). The annual limit for 2025 contributions is $4,300 for individuals and $8,550 for a family (an additional $1,000 catch up for anyone age 55 and up).

The HSA is great because contributions are tax-deductible, you can invest the funds for growth, and withdrawals for qualifying expenses are tax-free. You can also carry over contributions. It’s a “win-win-win” scenario.

Flexible Spending Account (FSA) Deadlines and Limits

An FSA is another type of account you can contribute to for medical expenses. Normally, you must use all the funds by December 31st. Your employer may allow for a grace period, which is typically three months.

In most cases, you'll need to enroll for next year as well to roll funds over. It's always best to use all funds if possible. You forfeit any money remaining in the account past the grace period.

Healthcare FSA

The 2025 healthcare FSA contribution limits were $3,300 with a maximum carryover of $660. Keep in mind that your employer determines whether any carryover is allowed. You can still submit reimbursement requests for the previous year for a limited time (usually 90 days).

Dependent Care FSA

Dependent care FSAs are similar, but have different limits. The DCFSA limit for 2025 was $5,000 per household or $2,500 per individual. The One Big Beautiful Bill Act increased it to $7,500 and $3,750 for 2026.

You generally have until March 15th to use funds the following year. So, all your 2025 funds must be used by that date.

College Savings Deadlines for 529 Accounts

If you’re saving for college for children, grandchildren, or yourself, the deadline for most states is December 31st. However, some states allow you to make contributions until April 15th. Contributions to 529 plans aren’t deductible at the federal level, but many states offer income tax deductions or credits.

Required Minimum Distributions

If you’re subject to required minimum distributions (RMDs), you normally have until December 31st to take the required distribution amounts. If not, you’ll be subject to a 25% penalty on the amount not withdrawn. This penalty can be reduced to 10% if corrected in a "timely" manner.

If you turned 73 in 2024, you’ll need to take your first RMD by April 1st, 2025 (or the year after you turn 73). In 2033, the RMD start age will increase to 75 due to changes under Secure Act 2.0.

QCD as an RMD

Keep in mind you can also use a qualified charitable contribution (QCD) to satisfy your RMD. If you’re already donating to charity and subject to RMDs, this could be a good strategy to save on taxes.

RMDs for Inherited IRAs

Inherited IRAs must have the RMDs taken by December 31st as well. These generally begin the year the original account holder passed away. The rules on inherited IRAs can be complicated, so be sure to consult your retirement team to ensure you don't get hit with a penalty.

How NextGen Wealth Tracks Important Deadlines

At NextGen Wealth, we use professional software to help us track all these important deadlines so our clients don’t miss anything. We also conduct regular reviews to ensure we maintain a complete understanding of what applies to you and what doesn’t. We’re huge fans of checklists, systems, and technology to help us be as efficient and thorough as possible.

If you'd like to see what working with NextGen Wealth looks like for you, contact us for your no-obligation financial assessment.

This article was written by

This article was written by