Compound Interest Can Be Your Ticket To Financial Freedom: Here’s How

Between student loan debt and the high cost of living, it can seem difficult to get ahead in this world. However, there’s an important concept that, when managed well, can accelerate the growth of your savings and increase your wealth like you couldn’t imagine. And, you’ve probably heard of it before; compound interest.

Hey, if Albert Einstein is calling compound interest the eighth wonder of the world, then you better take note!

When it comes to compound interest, time is on your side when it comes to investing and just the opposite when it comes to borrowing. If you’ve ever taken out a loan, you may have noticed that when you start making payments every month, the majority of the money goes toward interest. The longer your loan term, the longer it takes for your payments to go toward your principal balance.

On the flip side, though, the earlier you start investing and saving, the more that compound interest can make your financial freedom a reality. It’s a bold claim, but that is its true power. Before we put the cart before the horse, though, let’s start at the beginning.

What is compound interest?

Compound interest is the idea of money growing through a “snowball effect.” It’s the interest you earn on your interest, leading to your money growing at an accelerated pace. Sound a little complicated? Don’t worry, let us explain.

Let’s start with an example to make it easier to understand. If you deposit $200 in an account that pays 5% interest annually, you’ll have $210 at the end of that year.

This means you earned $10 in interest by keeping your money in the account. Imagine you just let the money sit in the account and don’t make any additional deposits.

At the end of year two, you’ll have $220.50. That means you earned 5% on the original deposit of $200 as well as on the $10 you earned through the interest payout in the first year – and this will continue year after year after year that the money remains invested in the account.

That’s the power of compound interest. As your initial balance grows, you’ll keep earning interest on your original deposit as well as on the interest you’ve already earned. This is sometimes known as exponential growth and it’s a key concept in building wealth.

If you’re trying to get your finances in order, you want to make compounding work for you by making quality investments. On the flip side, if you borrow money, compounding works against you because you’re the one paying the interest. In other words, you want to be an investor rather than a borrower to reap the rewards of compound interest.

The time value of money

The money you earn today has more value than the money you earn tomorrow. Why? Because you can invest it in an account that earns interest and increases in value with time.

For example, if you invest $100 in an account that earns 5% interest, in five years you’ll have $127.63. Let’s say you earn another $100 exactly five years from that date. The $100 you earn at that point will be worth $27.63 less than the $100 you earned five years ago because you didn’t earn any interest on it. This concept is called the time value of money and illustrates why compound interest is so valuable.

The most important take away is that the more you save and invest at a young age, the better off you’ll be in the long run. Compound interest takes time so it’s imperative you start putting your money to work for you as soon as possible. Save as much as you can by investing it and continue adding to it.

Every dollar you add to your accounts will continue to earn interest for as long as you have the account. The more money you put in, the faster it grows. Don’t miss out on tens of thousands of dollars in compound interest by getting a late start. Every day you delay costs you earned interest and lowers the future value of your account.

If you’re not sure how to put this to work for you, speak to a financial advisor who can help you get started on the right path. Getting your savings vehicles and loan repayment schedules figured out early means more money in your pocket over the long term. The earlier you start, the longer the time period for compound interest to work its magic.

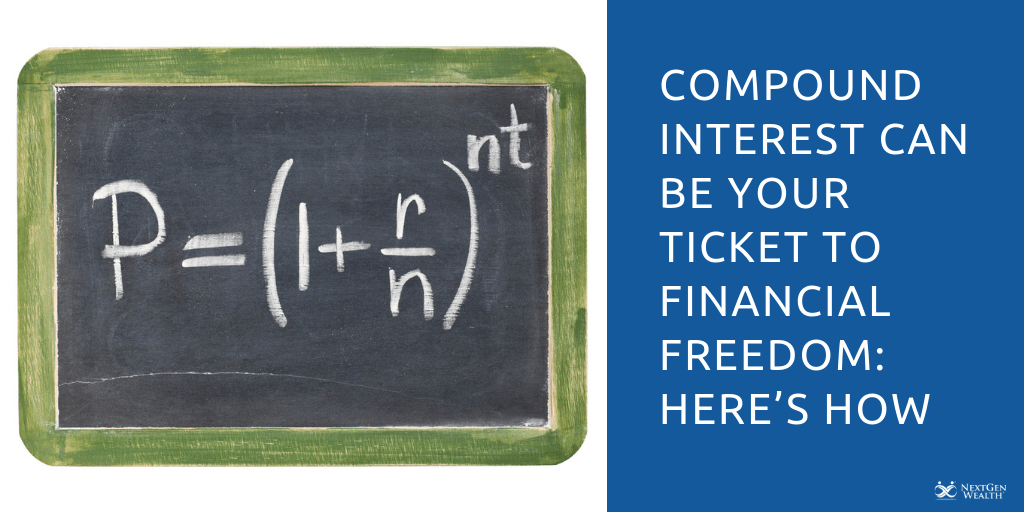

How to calculate compound interest

The formula used to calculate compound interest requires some math so if this section makes your eyes glaze over, feel free to use an online calculator (that’s what I do). As we discussed above, the simplest way to calculate compound interest is to multiply the previous year’s balance by the interest rate.

For example, if you invested $1,000 at 5% interest, after year one you’ll have $1,000 x 1.05 = $1,050. For year two, take last year’s balance ($1,050) and multiply by 5%, i.e. $1,050 x 1.05 = $1,102.5, and so on. However, this can get cumbersome if you’re trying to calculate multi-year compound interest returns. You can either use a calculator or the compound interest formula below:

A = P (1 + r/n) ^ n*t

Let’s go over each letter and what it means for the above equation: “A” refers to the final amount in the account after the number of years “t,” compounded “n” times at interest rate “r” with starting principal “P.” Here’s an example using the numbers above but for a 10-year investing horizon, compounded quarterly.

$1,000 (1 + 0.05/4) ^ (4*10) = $1,643.62

While it’s good to know how to calculate compound interest, there are plenty of online calculators that can do the job for you.

The rule of 72

Another way to quickly estimate compound interest is by using the rule of 72. It tells you what it takes to double your money with a given rate of return within a certain time period. All you have to do is divide 72 by your interest rate and the result will be how many years it will take you to double your money.

For example, if you have $1,000 invested in a savings account earning 5 percent as we did in the example above, how long will it take until you have $2,000? To figure it out, take 72 and divide it by the interest rate (5%), and you get 14.4. It will take you 14.4 years for your money to grow to $2,000 if you don’t add any more funds to the account.

Now that you know the basics, you can use them to plan out your future investment moves.

How to take advantage of compounding

While compound interest can have great advantages when used correctly, it can cost you thousands if you don’t use it properly. There are a few key ways to ensure compound interest works in your favor.

- Start early and save often – Remember in the example above how earning $100 five years later cost you $27.63 at a 5% interest rate? This means that the sooner you start saving, the more money you’ll have in the long run.

Save as much as possible today and keep adding to the balance every chance you get. Let compound interest do its thing and watch as your balance keeps growing year after year. It takes a while to build momentum but eventually, you’ll reap the benefits of saving early and often.

- Pay off debt quickly – Just like compound interest can work for you, it can also work against you. If you have debt, the principal amount of the debt is only a fraction of the payments you make every month. Interest accounts for most of your monthly payment, especially in the early days of repayment.

To minimize interest, pay extra every chance you can and try to pay off the loan as quickly as possible. Every dollar you put toward paying interest now will save you money in more interest over the long-term.

- Check the rate of return – When comparing savings accounts and CDs, make sure to compare the annual percentage yield (APY for short). Banks typically publicize the APY since it’s higher than the interest rate. It takes compounding into account and provides a true rate of return.

Check out different options for investing your money and keep in mind your investment time horizon. If you won’t need to access the funds for a while, a mutual may be a good option but if you think you need the money in the short-term, a high-yield savings account may better suit your needs, even if the interest rate will be lower.

- Lock in low borrowing rates – The interest rate on your loan determines how quickly you’ll repay the amount you borrowed along with what your monthly payment will be. Keep this in mind when borrowing money and try to get the lowest rate possible.

If your loan rate is higher than the rate of return you can get elsewhere, you’ll do better throwing all extra money toward paying off the loan. That’s why it’s important to lock in a low rate so you can put your extra cash toward accounts that will benefit from compound interest.

- Stay the course – Getting your accounts to grow through compound interest is slow at first. However, it starts to pick up quickly as exponential growth kicks in so it’s important to stay the course.

Don’t let the initial slow growth convince you that compound interest isn’t worth the hassle. If that was the case, banks wouldn’t lend out money. Stay the course and keep adding money to your accounts and soon enough you’ll start seeing your hard work pay off.

Beware of the downsides

As noted earlier, compound interest can work for or against you. If you have ever taken out a loan, you may have noticed that you end up paying back much more than the original loan. Just like compound interest builds your savings over time, it also works the other way, building your loan balances.

That’s why deferring loan repayment can have such a detrimental effect. If you stop making payments on your loans, the balance will continue to grow month after month. The larger the loan balance, the faster it will grow. It’s important to continue making payments on all of your loans and to accelerate repayment as much as possible.

Another important downside is delaying saving for retirement. Opening a retirement account at an early age and setting money aside every month is critical for retiring on time. If you delay even a few years, you’ll be forfeiting thousands if not tens of thousands of dollars of future earnings through the magic of compound interest.

Keep your lifestyle inflation in check and instead put extra money toward retirement and savings accounts that will ensure your future financial stability.

Watch out for inflation

Another key point to remember is that inflation will erode your returns. Looking at inflation rates over the last few years, it’s important to account for a 3 to 4 percent rate of inflation when calculating your savings. The value of $1 today is not the same as the value of $1 in five years. This means your returns are eroded if your account isn’t growing.

When researching interest rates, try to find inflation-beating rates. Depending on the current investment climate, that may not be possible. However, try to find the highest possible interest rate for your savings and keep adding to the account. Over time, your money will begin to grow faster, eventually outpacing inflation.

Set yourself up for success

While your earnings from compound interest can be slow-going at first, the amount will grow rapidly as you keep adding to your accounts. Don’t let the initial slow growth discourage you from putting your money in interest-earning savings vehicles. Also, make sure you’re investing in mutual funds for your longer-term goals and don’t forget to keep adding money to your retirement accounts.

Talk to a trusted financial advisor about how to allocate your savings to account for inflation and take advantage of maximum yield. Get your finances in order to set yourself up for financial success.

Keep in mind that compound interest can work both for you and against you. It’s up to you how you use your hard-earned dollars to invest in your long-term success.

This is a post from Clint Haynes, a Certified Financial Planner® and Financial Advisor in Kansas City, Missouri. He is also the founder and owner of NextGen Wealth. You can learn more about Clint at the website NextGen Wealth.

This article was written by

This article was written by