Most of us like to know the length of time it will take our investment to grow. We want all the numbers: estimates, figures, how old we will be when it’s doubled, etc. Some things in life are just hard to know because there are no guarantees.

But with the Rule of 72, you always know the number of years it takes to double an investment. The Rule of 72 will tell you a lot about the money you invest. Thanks to the Rule of 72, the table below tells us how many years it will take an initial $10,000 investment to double, depending on the rate of return.

|

Years |

3% |

6% |

12% |

|

0 |

$10,000 |

$10,000 |

$10,000 |

|

6 |

$20,000 |

||

|

12 |

$20,000 |

$40,000 |

|

|

24 |

$20,000 |

$40,000 |

$160,000 |

|

36 |

$80,000 |

$320,000 |

|

|

48 |

$40,000 |

$160,000 |

$2,560,000 |

What is the Rule of 72?

The Rule of 72 is a formula used to estimate the number of years it will take to double your money invested at a particular rate of return. It’s just a quick and easy method to get an idea of what your money might be worth over time.

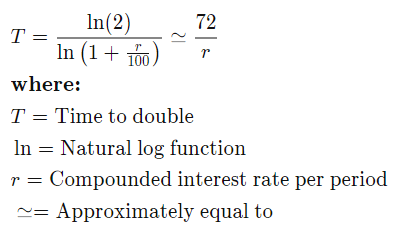

The Formula for the Rule of 72

Calculators and formulized spreadsheets can give you this number pretty quickly once the proper numbers are inputted. But for those of us who don’t have those luxuries, the formula for the Rule of 72 is:

Years to Double =72 ÷ Interest Rate (rate of return on investment)

How to Use the Rule of 72

The Rule of 72 is a good tool to learn the number of years it takes money to double your money in just about any situation, like your investments, the population, the gross domestic product (GDP), or the loans we borrow. For example, if the GDP grows annually at 4%, it’s expected the economy will double in 18 years (72÷4=18).

Let’s use inflation as a different type of example on how to use the Rule of 72. If inflation is 6%, your money will be worth half as much of what it is now in 12 years. How do we know? Because 72÷6=12. Likewise, if inflation goes down from 6% to 4%, your money will lose half of its value in 18 years.

Like most people, you want to see how your money grows. To see this for yourself, the Rule of 72 is one of the best places to start.

It’s necessary to note the Rule of 72 assumes that every time you receive interest in an investment, you are reinvesting that money i.e. compound interest. In this way, your interest is working to earn more interest for you. And the process continues.

Using the Rule of 72 is a practical way to make decisions about your money. If you understand it, you can apply it to just about anything, and you’ll be less likely to fall for gimmicky promotions that banks offer or settle for solutions that don’t give you an advantage.

The Rule of 72 is used in situations when you are accruing compound interest. Compound interest helps earn you more money faster. So, what exactly is compound interest?

What is Compound Interest?

There’s a cost to borrow money. And that amount it costs you to borrow, which is money you pay in addition to what you borrowed is called interest. Interest is also the money you may receive from money you’ve invested.

Interest is always in addition to the principal amount. Interest can be calculated in two ways: simple interest or compound interest.

Simple interest is a basic calculation of the principal or original loan amount. The interest is compounded when the calculation includes the original principal and accumulated interest of previous periods. In essence, compound interest is interest on interest.

The rate the compound interest earns depends on how often it’s compounded. The more compounding periods there are, the more interest earned

The History of the Rule of 72

The concept of the Rule of 72 was first introduced in 1494 by an Italian mathematician named Luca Pacioli. Pacioli mentioned the importance of the number 72 in his book, Summary of Arithmetic, Geometry, Proportions, and Proportionality.

According to Pacioli, you could use the number 72 to determine the number of years it would take to double your money. A century later, the actual formula was developed, based on a basic compound interest formula.

The bottom line is, after a very complex formula, the outlining number to base the calculation on was determined to be 69.3, not 72. However, since 69.3 is a difficult number to divide into, statisticians decided to use the next best integer, 72. This gives a more approximate time it will take to double your investment.

While some investors may still prefer to use 69.3 for maximum accuracy, the Rule of 72 is still a good option and the most convenient formula for calculating the number of years it takes your money to double.

How accurate is the Rule of 72?

The Rule of 72 provides a reasonably accurate and approximate response to knowing how many years it would take an investment (or other factors) to double. There is a more complex algorithm that is applied, but this formula is a simple version of it that allows the average Joe or Jane to figure it out without needing to go through the complex equation.

However, that more complex equation is:

Using the same number, one answer may be 9.006 years, the other (simpler equation) maybe nine years. We’ll let you decide which equation you would prefer to use.

Variations of the Rule of 72

The Rule of 72 is a great formula for determining equations of this type. However, it is most accurate at an 8% interest rate. It is still good for calculating any percentage from 4% to 15% though.

Beyond those amounts, it may get a little suspect. That said, there are a few ways to make it more accurate using a basic math equation.

For every three points an interest rate is from 8%, adjust the number 72 by one in the direction the rate is changing. For instance, if the rate is 5%, take one point off the rule and lower the rule to 71.

If the rate increases by three points to 11%, increase the rule to 73. A 14% rate would increase the rule to 74. The table helps to better understand how to adjust the basic formula for the Rule of 72.

|

Interest Rate (%) |

Points from 8% |

Adjustment to the ‘72’ |

Adjusted Formula |

Years to Double |

|

14 |

6 |

72+2=74 |

74÷14=5.29 |

5 years |

|

11 |

3 |

72+1=73 |

73÷11=6.64 |

7 years |

|

5 |

(3) |

72-1=71 |

71÷5=14.2 |

14 years |

What About The Rules of 72, 69.3, or Just 69?

Rules of 69.3 and 69 are also known methods for estimating the number of years it would take money to double. While the rule of 69.3 is considered to be more accurate for determining these numbers, it is not as simple a formula as the Rule of 72.

A comparison chart shows the similarity of the three different calculations. This explains why it’s just simpler to use 72.

|

Interest Rate (%) |

Using 72 |

Using 69.3 |

Using 69 |

Number of Years to Double |

|

1 |

72 |

69.3 |

69 |

69.66 |

|

3 |

24 |

23.10 |

23 |

23.45 |

|

5 |

14.40 |

13.86 |

13.80 |

14.21 |

|

10 |

7.20 |

6.93 |

6.90 |

7.27 |

Conclusion

Your life only has a limited number of doubling periods, As the Rule of 72 shows us, the higher the interest rate, the less time it will take for money that‘s based on compounded interest to double.

The thing is, it’s not always easy to get the higher rates, so for most of us, it takes our money quite a while to work for us. How is your money working for you? Would a free financial assessment help you see how your money is stacking up, or if you’ve taken on some financial responsibilities or loans that don’t work in your favor?

NextGen Wealth is dedicated to ensuring that your financial plan works in favor of your financial goals. Your financial plan should serve as the basis for all other financial decisions that you make.

Do you have a plan in place? Without a plan you don’t know where you’re going, nor do you know when you’ve arrived at what you’re after.

You need to know how much you need to be saving for retirement. You need to know how much money you will need in retirement. Working with a financial planner is a way to get started with knowing what you need.

Let’s get the process started today. We’re only a click away!